Last Updated: 02 June 2026

For millions of Americans, Social Security is more than a monthly payment-it is a key source of income that helps cover everyday expenses.

That is why annual Cost-of-Living Adjustments (COLA) receive so much attention. A higher COLA can help retirees keep up with rising prices, while a smaller increase can make it harder to manage essential costs.

Most retirees already expect a COLA increase. The bigger concern is whether that increase will actually cover rising costs. The real concern is whether that adjustment will be enough to offset rising expenses such as healthcare, housing, insurance, and groceries.

Knowing these potential risks now can help retirees avoid budget surprises later.

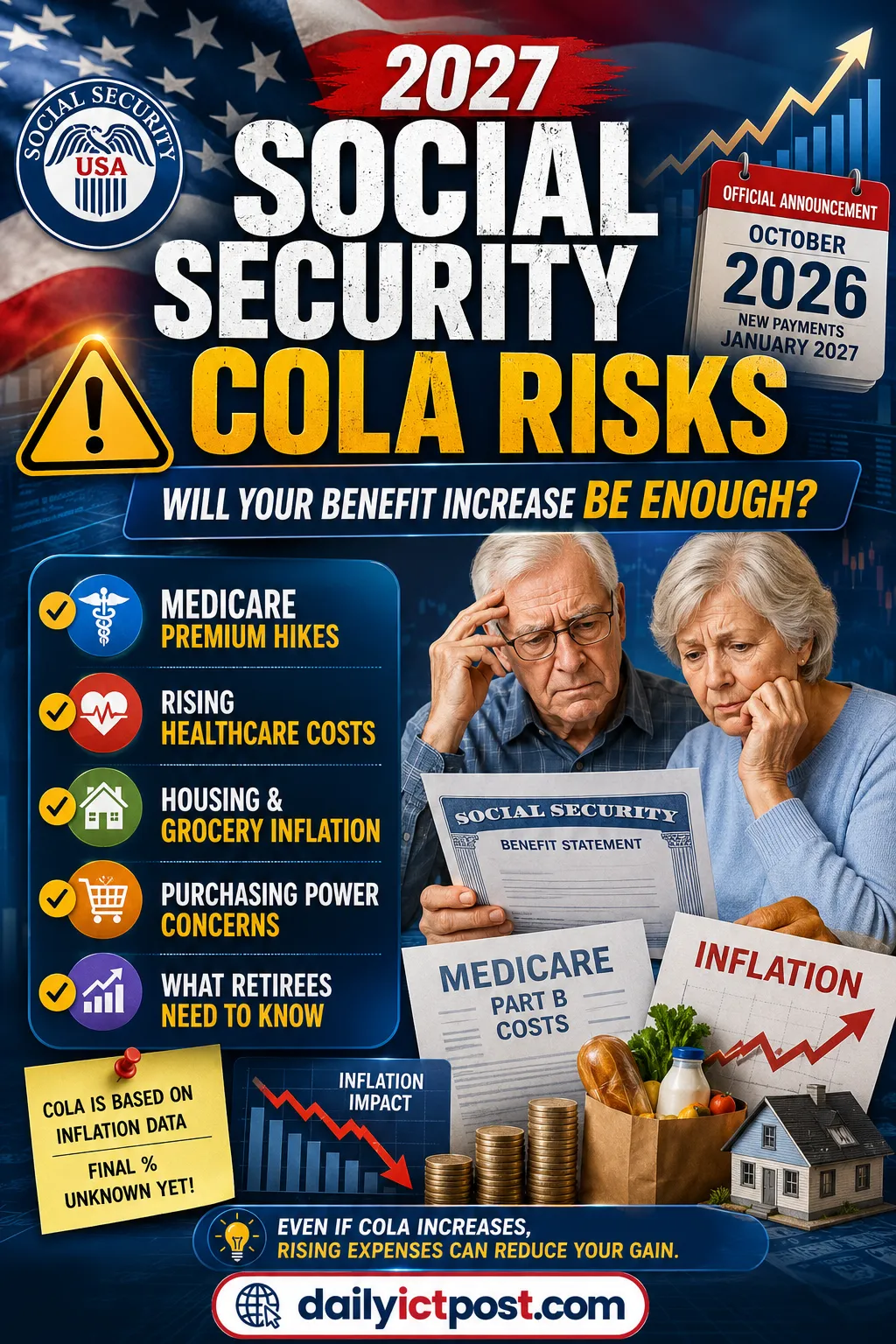

Quick Overview: 2027 Social Security COLA Risks

- Official 2027 COLA has NOT been announced yet

- COLA is expected to depend on 2026 inflation data

- Medicare premium increases could reduce actual benefit gains

- Healthcare and housing costs remain major concerns

- The Official COLA announcement is typically released in October 2026

- New payment amounts usually begin in January 2027

Bottom line: Even if COLA increases, retirees should prepare for rising expenses that may offset part of the gain.

Editorial Disclaimer:

This article is for informational and educational purposes only.

The official 2027 Social Security COLA has not yet been announced by the Social Security Administration (SSA). Any references to potential COLA outcomes, inflation trends, or financial impacts are based on publicly available economic data, historical trends, and expert analysis available at the time of writing.

Readers should verify all information through official government sources, including SSA.gov and Medicare.gov, before making financial or retirement planning decisions.

Key Takeaway: The official 2027 COLA percentage has not yet been announced. This article discusses potential risks and financial planning considerations based on historical COLA trends, inflation data, and publicly available government information.

Who Should Pay Attention to 2027 COLA Risks?

This guide is especially useful for:

- Social Security retirees

- SSI recipients

- SSDI beneficiaries

- Medicare beneficiaries

- Near-retirees planning for 2027

- Seniors living primarily on a fixed income

What Is Social Security COLA and Why Does It Matter?

Social Security COLA is an annual adjustment intended to help benefits keep pace with inflation.

Without these increases, the purchasing power of Social Security benefits would gradually decline as prices rose. Even moderate inflation can have a noticeable impact on households that depend heavily on fixed income.

For many retirees, Social Security covers a significant share of monthly living expenses. As a result, even small changes in the annual COLA can affect household budgets.

Check it out: USA Government Benefits Resources

How COLA Is Determined

The Social Security Administration uses inflation data from the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W).

The average inflation rate for the third quarter is compared with a previous benchmark period. If inflation increases, benefits typically rise the following January.

Beneficiaries do not need to apply for the adjustment because it is calculated automatically.

Social Security payment schedule: Confirmed Official June 2026 SSA Payments Schedule: Shocking Changes for SSI; SSDI Recipients

Key 2027 Social Security COLA Risks

Several factors could affect how much value beneficiaries actually receive from a 2027 COLA increase.

Quick Overview

| Risk Factor | Potential Impact |

|---|---|

| Lower Inflation Readings | Smaller COLA increase |

| Higher Healthcare Costs | Benefits may not keep pace |

| Medicare Premium Growth | Reduces net benefit gains |

| Housing Cost Pressure | Increased financial strain |

| Food and Utility Inflation | Lower purchasing power |

| Economic Uncertainty | Greater reliance on Social Security |

Risk #1: COLA May Not Match Retirees’ Real Expenses

One of the most common concerns among retirees is that official inflation measurements do not always reflect their actual spending patterns.

Older Americans often spend a larger portion of their income on healthcare, prescription drugs, insurance, and long-term care. These costs can rise faster than overall inflation.

As a result, a COLA increase that looks reasonable on paper may not fully cover the higher expenses many retirees face throughout the year.

This gap between official inflation data and real-life expenses remains one of the most discussed Social Security COLA concerns.

SSI benefits: SSI Benefits Warning 2026: The Mistakes That Could Cost You Your Check

Risk #2: Medicare Premium Increases Could Offset COLA Gains

A COLA increase does not necessarily mean beneficiaries will have significantly more money available each month.

Medicare Part B premiums are typically deducted directly from Social Security benefits. If those premiums increase, they can reduce the amount beneficiaries actually receive.

Example Scenario

| Item | Amount |

|---|---|

| Monthly Benefit Before COLA | $2,000 |

| 3% COLA Increase | +$60 |

| Medicare Premium Increase | -$25 |

| Net Monthly Gain | $35 |

This is why many retirees pay close attention to both COLA announcements and Medicare premium updates.

Risk #3: Housing Costs May Continue Rising

Many retirees expected housing costs to stabilize after recent inflation cooled. However, property taxes, insurance premiums, HOA fees, and maintenance expenses continue to rise in many parts of the country, creating additional pressure on fixed-income households.

Even homeowners can face increasing costs through property taxes, insurance premiums, repairs, maintenance, and utility bills. Renters may also experience higher monthly housing expenses.

If housing costs continue to rise faster than inflation, a modest COLA increase may provide limited relief.

Retirees living on fixed incomes often feel these increases more than working households because they have fewer opportunities to offset higher costs with additional income.

A 3% COLA increase may sound significant, but retirees often experience higher increases in healthcare, insurance, and housing expenses than the overall inflation rate used for COLA calculations.

Medicare premium updates: How to Renew Medicaid USA 2026 Fast: Guide to Guaranteed Coverage

What Financial Experts Watch Before Every COLA Announcement

Financial analysts typically monitor several indicators before the annual COLA announcement:

- CPI-W inflation data

- Medicare premium projections

- Housing inflation trends

- Energy price fluctuations

- Healthcare cost growth

While no forecast is guaranteed, these indicators often provide clues about future COLA adjustments.

Continue Reading: SSI Payment Boost 2026: New SSI Increase, Eligibility & Payment Changes

Historical Social Security COLA Performance

| Year | COLA |

|---|---|

| 2020 | 1.6% |

| 2021 | 1.3% |

| 2022 | 5.9% |

| 2023 | 8.7% |

| 2024 | 3.2% |

| 2025 | 2.5% |

| 2026 | 2.5% |

The sharp increase in 2023 was largely driven by unusually high inflation, while recent years have shown a return toward more moderate adjustments.

Inflation Trends That Could Influence the 2027 COLA

The final 2027 COLA will depend largely on inflation trends during the measurement period.

Several economic factors could influence the adjustment amount.

| Economic Trend | Possible COLA Effect |

|---|---|

| Cooling Inflation | Smaller adjustment |

| Persistent Services Inflation | Higher adjustment |

| Energy Price Volatility | Uncertain impact |

| Wage Growth | Potential inflation pressure |

| Supply Chain Disruptions | Higher consumer prices |

While forecasts can provide clues, the official COLA calculation depends on actual inflation data rather than predictions.

See more: [Good News for Seniors] Best Supplemental Security Income Eligibility Guide 2026

How a Small COLA Could Affect Retirees

A smaller COLA can create budgeting challenges for households already dealing with rising expenses.

The impact is often felt most in categories that tend to increase regularly, regardless of overall inflation trends.

Areas Most Likely to Be Affected

- Grocery expenses

- Prescription medications

- Utility bills

- Transportation costs

- Insurance premiums

- Long-term care services

Retirees with limited savings may need to adjust spending priorities if expenses increase faster than benefit payments.

What If Inflation Accelerates Again Before 2027?

If inflation unexpectedly rises during the measurement period, beneficiaries could receive a larger COLA adjustment. However, higher inflation often increases healthcare, housing, food, and utility costs simultaneously.

As a result, a larger COLA does not always translate into greater purchasing power.

Comparing Recent COLA Trends

Looking at recent COLA increases helps provide context for what retirees might expect in future years.

| Year | COLA Increase |

|---|---|

| 2023 | 8.7% |

| 2024 | 3.2% |

| 2025 | 2.5% |

| 2026 | 2.5% |

What This Trend Suggests

The unusually large adjustment in 2023 was driven by historically high inflation.

Since then, inflation has moderated, leading to smaller COLA increases that are closer to long-term averages.

While future inflation remains uncertain, retirees should avoid assuming that exceptionally large COLA increases will continue.

Who Could Be Most Affected by a Smaller 2027 COLA?

Some groups may feel the impact of a smaller COLA more than others:

- Retirees relying primarily on Social Security

- Individuals with chronic healthcare expenses

- Seniors renting rather than owning a home

- Beneficiaries with limited retirement savings

- Older adults facing long-term care costs

Many retirees focus only on the announced COLA percentage. In reality, the amount that reaches your bank account after Medicare deductions often matters more than the headline number itself.

Financial Planning Strategies for 2027

Preparing for uncertainty is often more effective than predicting the exact COLA amount.

Review Monthly Expenses

Take time to review spending habits and identify categories that have increased over the past year.

Healthcare, insurance, utilities, and food costs are often worth monitoring closely.

Regular budget reviews can make it easier to adapt when expenses change.

Build an Inflation Buffer

An emergency fund can help absorb unexpected cost increases.

Even a modest reserve can provide flexibility when living expenses rise faster than expected.

Evaluate Healthcare Costs

Healthcare is often one of the fastest-growing expenses during retirement.

Reviewing available coverage options and comparing plans during enrollment periods may help reduce future costs.

Read more: Social Security Retirement Benefits

Avoid Overestimating Future COLA Increases

Many retirees make financial decisions based on expected benefit growth.

A more conservative approach can help prevent budgeting problems if future COLA increases are smaller than anticipated.

Common Mistakes Beneficiaries Make

Assuming COLA Automatically Improves Financial Security

A higher monthly benefit does not always translate into greater purchasing power.

Rising expenses can absorb much of the increase.

Ignoring Medicare Changes

Focusing only on the COLA percentage can create unrealistic expectations about future benefit payments.

Medicare costs should always be considered alongside benefit adjustments.

Skipping Annual Budget Reviews

Living expenses change over time.

Reviewing a household budget each year helps identify potential financial pressures before they become larger problems.

Depending Entirely on Social Security

For retirees with additional savings or retirement income sources, diversification can provide greater financial stability during periods of inflation.

Quick Facts About 2027 Social Security COLA Risks

| Fact | Details |

|---|---|

| COLA Is Automatic | No application required |

| Based on Inflation Data | Uses CPI-W measurements |

| Healthcare Costs Matter | Often rise faster than overall inflation |

| Medicare Can Reduce Gains | Premium increases affect net benefits |

| Exact 2027 COLA Unknown | Determined after inflation data is finalized |

| Planning Ahead Helps | Budget preparation reduces financial stress |

Timeline: When COLA Information Is Usually Released

| Period | Typical Activity |

|---|---|

| July–September 2026 | Inflation measurement period |

| October 2026 | Official COLA announcement |

| December 2026 | Updated benefit notices |

| January 2027 | New payment amounts begin |

Expert Tip

When evaluating a future COLA increase, focus on the amount that will actually reach your bank account after Medicare deductions and rising living expenses.

That number provides a more realistic picture of how much your financial situation may improve.

What We Know vs What We Don’t Know Yet

What We Know

- COLA is based on CPI-W inflation dataTheThe

- October 2026 announcement is expected

- January 2027 payments will reflect the new COLA

What We Don’t Know Yet

- Exact 2027 COLA percentage

- Final Medicare Part B premium changes

- Future inflation levels through the measurement period

Sources Used In This Analysis

- Social Security Administration (SSA)

- Bureau of Labor Statistics (BLS)

- Medicare.gov

- Historical COLA data published by SSA

FAQs

What is the biggest 2027 Social Security COLA risk?

The biggest risk is that the COLA increase may not fully keep up with rising costs such as healthcare, housing, insurance, and everyday living expenses.

Will Social Security benefits increase in 2027?

If inflation rises during the measurement period used by Social Security, beneficiaries will likely receive a COLA increase. The exact percentage will not be known until official data is released.

Can Medicare premium increases reduce my COLA benefit?

Yes. Higher Medicare Part B premiums can reduce the amount of additional income beneficiaries receive from a COLA adjustment.

When will the 2027 COLA be announced?

The Social Security Administration typically announces the annual COLA in October.

Does every beneficiary receive the same COLA percentage?

Generally, the same percentage increase applies to Social Security retirement, disability, and survivor benefits.

How can retirees prepare for COLA uncertainty?

Review household expenses regularly, maintain emergency savings, monitor healthcare costs, and avoid relying on projected benefit increases when creating a budget.

Final Verdict

The biggest 2027 Social Security COLA risks are tied to purchasing power rather than the adjustment itself.

Even if benefits increase, retirees may still face pressure from rising healthcare costs, Medicare premiums, housing expenses, and everyday inflation.

The most effective strategy is to prepare for multiple scenarios, monitor spending carefully, and treat COLA increases as one part of a broader retirement income plan. Beneficiaries who stay proactive and flexible will be in a stronger position regardless of the final 2027 COLA percentage.

")

")

![[Confirmed] New Social Security Changes in June 2026 - Important Changes Retirees Need to Know](https://dailyictpost.com/wp-content/uploads/2026/06/Confirmed-New-Social-Security-Changes-in-June-2026-Important-Changes-Retirees-Need-to-Know-150x150.webp "[Confirmed] New Social Security Changes in June 2026 | Important Changes Retirees Need to Know")