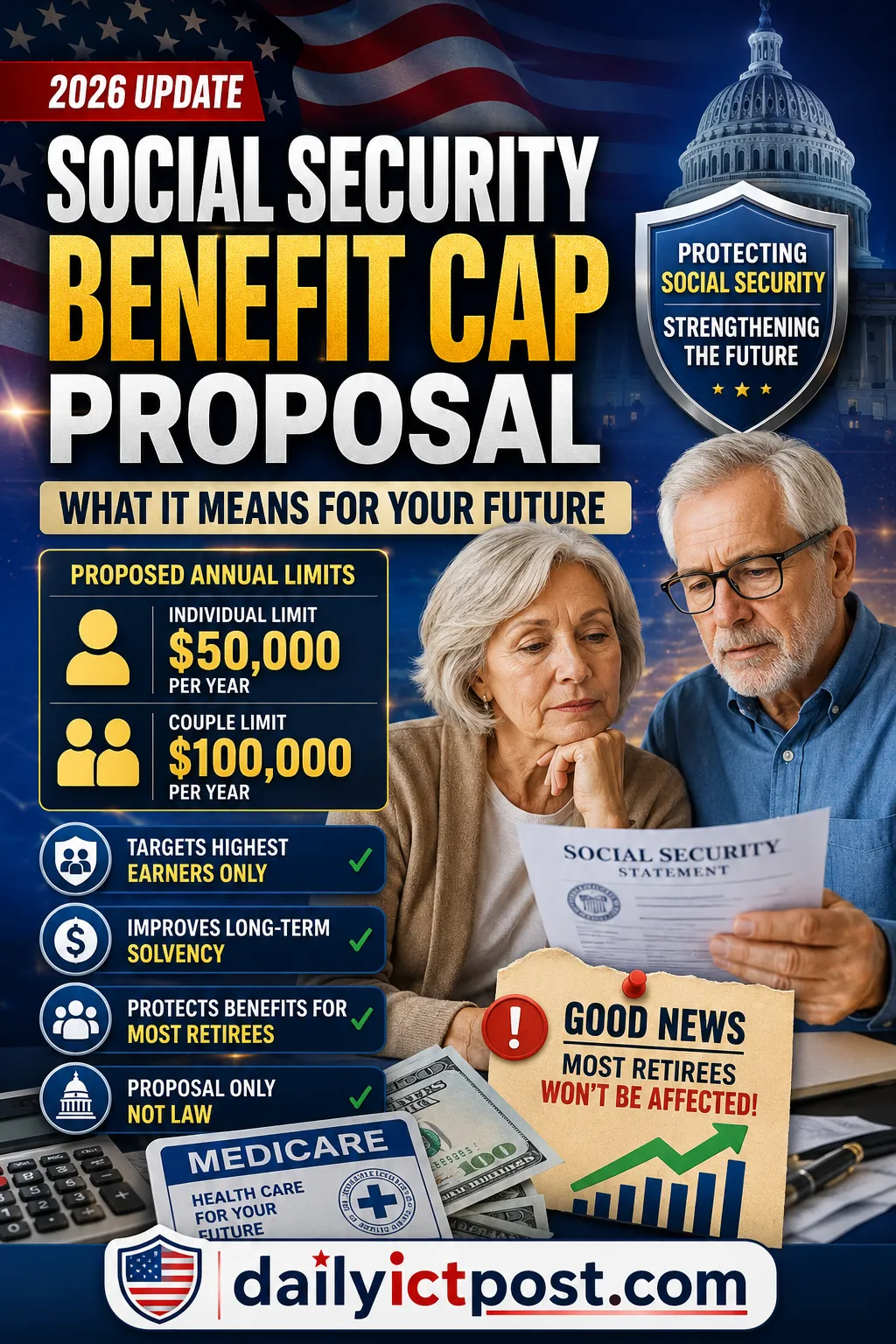

The social security benefit cap proposal has become one of the most talked-about ideas in the debate over the future of Social Security.

The proposal does not reduce benefits for average retirees. Instead, it focuses on limiting extremely large Social Security payments received by a small number of high-income retirees.

Fiscal policy organizations and budget analysts have explored several approaches to improving Social Security solvency. One proposal focuses on limiting exceptionally large retirement benefits while preserving scheduled payments for the overwhelming majority of beneficiaries. Supporters view this as a targeted adjustment, while opponents argue it changes the long-standing relationship between payroll contributions and retirement benefits.

At this stage, the social security benefit cap proposal is only a policy idea. Congress has not approved it, and no changes have been made to current Social Security benefits.

Quick Overview: Social Security Benefit Cap Proposal Explained for 2026

Current status

Proposal only (not law)

Proposed individual limit

$50,000 annually

Proposed couple limit

$100,000 annually

Average retirees affected

Unlikely

Main goal

Improve Social Security solvency

Congressional approval

No

Current benefits impacted today

No

✔

Expert Review & Editorial Notice

Last Updated: 04 July 2026

Author Experience

This article was reviewed using publicly available information from the Social Security Administration (SSA), Congressional Budget Office (CBO), and federal budget policy

research organizations. It is intended for educational purposes only and

does not constitute legal, financial, retirement, or tax advice.

Editorial Disclaimer

This article is independently researched and written for informational

and educational purposes only.

It does not constitute legal, tax, investment, retirement, or financial

advice and should not replace guidance from the Social Security Administration,

financial advisors, tax professionals, or government agencies.

Social Security legislation, benefit formulas, funding projections, and

congressional proposals may change over time.

Readers should verify all information through official government sources

before making retirement or financial decisions.

This article discusses policy proposals and public discussions only.

Unless officially enacted by Congress and signed into law, proposals

discussed in this article do not affect current Social Security benefits.

Key Takeaways

✔ The proposal is not law.

✔ Current retirees continue receiving benefits under existing rules.

✔ The proposal mainly targets exceptionally high lifetime earners.

✔ Congress has not introduced legislation to implement the proposal.

✔ Most retirees would likely never be affected.

Social Security Benefit Cap Proposal Explained for 2026

Why Was the Social Security Benefit Cap Proposal Created?

Social Security faces long-term financial pressure as Americans live longer and the ratio of workers to retirees continues to decline.

Current projections show that without legislative action, Social Security may eventually be unable to pay full scheduled benefits from dedicated revenue alone.

Supporters of the social security benefit cap proposal argue that limiting very large benefits could help preserve the program without reducing payments for most retirees.

Supporters argue that if lawmakers ever make changes, protecting average retirees while slowing benefit growth for only the highest earners could be one way to reduce pressure on the system.

Why Are Some Retirees Already Receiving Six-Figure Benefits?

Social Security benefits are based on lifetime earnings and the age when benefits begin.

Workers who earn at or above the taxable wage limit for at least 35 years and delay retirement until age 70 can qualify for extremely large monthly checks.

In 2026, the maximum Social Security benefit for someone claiming at age 70 is $5,181 per month, or more than $62,000 annually.

When both spouses qualify for maximum benefits, combined household payments can exceed $100,000 per year.

Other Social Security Reform Ideas Being Discussed

Several Social Security reform proposals continue to be discussed by lawmakers and policy experts as the program faces long-term funding pressure.

Raise the payroll tax cap: Apply Social Security taxes to earnings above the current taxable wage limit so higher earners contribute more.

Increase the retirement age: Gradually raise the full retirement age to reflect longer life expectancy.

Modify the COLA formula: Change how annual cost-of-living adjustments are calculated.

Increase the payroll tax rate: Raise the Social Security payroll tax percentage for workers and employers.

Means testing: Reduce benefits for higher-income retirees while protecting lower-income beneficiaries.

According to the latest projections from Social Security Administration Trustees Reports, policymakers are discussing multiple options because the program’s trust funds face long-term financial challenges. None of these proposals has become law, but they remain part of ongoing reform discussions.

Potential Advantages of the Social Security Benefit Cap Proposal for Long-Term Solvency

Supporters say the social security benefit cap proposal offers several benefits.

Potential Advantages of the Social Security Benefit Cap Proposal for Long-Term Solvency

Improved Long-Term Solvency

Supporters believe this approach could modestly reduce long-term funding pressure and buy additional time for broader Social Security reforms.

Protection for Most Retirees

Because the proposal targets only the highest earners, most retirees would continue receiving full scheduled benefits.

Lower Risk of Across-the-Board Cuts

If lawmakers fail to act, future benefit reductions could affect all retirees. Some experts believe targeted reforms may help avoid that outcome.

Why Some Economists and Retirees Oppose the Proposal

Not everyone supports the proposal.

Critics argue that Social Security has always linked benefits to lifetime contributions.

Workers who paid the maximum payroll taxes for decades may view benefit limits as unfair.

Others worry that once benefit caps are introduced for wealthy retirees, lawmakers could later expand them to additional income groups.

Is the Social Security Benefit Cap Proposal Becoming Law?

No.

The social security benefit cap proposal has not been introduced as federal law and has not been approved by Congress.

Any future changes would require:

Introduction of legislation.

Approval by Congress.

Signature by the President.

Because none of these steps have happened, current retirees will continue receiving benefits under existing rules.

Why Social Security Reform Discussions Are Increasing in 2026

Social Security reform discussions are growing in 2026 because the U.S. population is aging rapidly. At the same time, the worker-to-retiree ratio continues to decline, meaning fewer workers are supporting more beneficiaries through payroll taxes.

Another concern is increasing pressure on the Social Security trust funds. According to the latest Trustees Report from the Social Security Administration Trustees Reports, the retirement trust fund could face reserve depletion around 2032 if no changes are made. Demographic shifts and longer life expectancy are major reasons policymakers continue discussing reform options.

How This Proposal Differs From Raising The Payroll Tax Cap

Two major Social Security reform ideas receive the most attention:

Reform Idea

Affected Group

Payroll Tax Cap Increase

High earners during working years

Benefit Cap Proposal

High earners during retirement

A payroll tax cap increase would raise taxes on higher-income workers. A benefit cap proposal would instead limit very large retirement benefits paid in the future.

Could Similar Proposals Appear In Future Congressional Bills?

No similar proposal has been introduced as law at this time. However, future deficit reduction discussions could revisit benefit limits or other Social Security reforms.

Bipartisan commissions and policy groups frequently examine benefit formulas, retirement ages, and funding options as long-term solvency concerns continue.

What Would Happen To Existing Retirees If Such A Law Passed?

If a future law were approved, several approaches could be considered:

Existing retirees could be grandfathered into current rules.

Changes might apply only to future retirees.

Benefits could be phased in gradually over several years.

Congress has historically used phased implementation when making major retirement policy changes.

How Likely Is This Proposal To Become Law?

Factor

Probability

Congressional support

Low

Public support

Mixed

Fiscal pressure

High

Near-term enactment chance

Low

While fiscal pressure on Social Security continues to increase, there is currently no indication that such a proposal is close to becoming law.

Possible Timeline if Congress Ever Approved a Benefit Cap

Proposal introduced in Congress.

House approval.

Senate approval.

Presidential signature.

Multi-year implementation period.

Have Social Security Benefit Rules Changed Before?

Yes.

Congress has previously changed:

Full retirement age

Payroll tax limits

Cost-of-living formulas

Taxation of benefits

Major Social Security reforms have historically been phased in gradually over many years.

Official Government Resources

Readers can verify Social Security information using official government resources:

Is the social security benefit cap proposal already approved?

No. Congress has not approved any nationwide Social Security benefit cap.

Will current retirees lose benefits?

Current retirees continue receiving benefits under existing law.

Who would be affected the most?

Retirees receiving the largest Social Security benefits would be most affected.

Why are lawmakers discussing benefit caps?

The discussion is part of broader efforts to strengthen Social Security finances for future generations.

Where can I check my estimated Social Security benefits?

You can view your earnings history and benefit estimates through the official Social Security Administration website.

Conclusion

The social security benefit cap proposal is aimed at a very small group of high-income retirees rather than average Americans.

Its supporters see it as a way to improve Social Security finances without reducing benefits for most households. Critics believe it weakens the connection between contributions and benefits.

Most importantly, the proposal is not law and has not been approved by Congress.

For now, Americans should continue planning retirement based on current Social Security rules while monitoring future policy developments.

The dailyictpost.com team presents job recruitment notices, various government and private job question solutions, government post activities and technology-based information in simple and practical language. Along with this, we explain ICT, mobile, computer, apps, online income, digital tools, government services, national elections and cyber security-related issues in such a way that the reader can understand and learn.

We believe that learning technology is not difficult, if it is explained correctly. Therefore, we present complex topics like using new software, mobile settings or digital marketing step by step in such a language that it feels like someone is sitting next to you and explaining it in a simple way.

Our goal is only one - that the reader gets accurate information, learns with confidence and can use that knowledge in real life.

![[Trending News] Social Security Insolvency Reform Proposals for 2026](data:image/svg+xml;base64,PHN2ZyB4bWxucz0iaHR0cDovL3d3dy53My5vcmcvMjAwMC9zdmciIHdpZHRoPSIxNTAiIGhlaWdodD0iMTUwIiB2aWV3Qm94PSIwIDAgMTUwIDE1MCI+PHJlY3Qgd2lkdGg9IjEwMCUiIGhlaWdodD0iMTAwJSIgc3R5bGU9ImZpbGw6I2NmZDRkYjtmaWxsLW9wYWNpdHk6IDAuMTsiLz48L3N2Zz4= "[Trending News] Social Security Insolvency Reform Proposals for 2026")

![[Trending News] Social Security Insolvency Reform Proposals for 2026](https://dailyictpost.com/wp-content/uploads/2026/06/Trending-News-Social-Security-Insolvency-Reform-Proposals-for-2026-150x150.webp "[Trending News] Social Security Insolvency Reform Proposals for 2026")

Explained: Average Benefits Now $2,071")

![[Confirmed] New Social Security Changes in June 2026 - Important Changes Retirees Need to Know](https://dailyictpost.com/wp-content/uploads/2026/06/Confirmed-New-Social-Security-Changes-in-June-2026-Important-Changes-Retirees-Need-to-Know-150x150.webp "[Confirmed] New Social Security Changes in June 2026 | Important Changes Retirees Need to Know")

![[UPDATED] Don’t Miss Your Exact Date - MAY Social Security Payment Schedule 2026 in the USA Revealed](https://dailyictpost.com/wp-content/uploads/2026/04/UPDATED-Dont-Miss-Your-Exact-Date-MAY-Social-Security-Payment-Schedule-2026-in-the-USA-Revealed-150x150.webp "[UPDATED] Don’t Miss Your Exact Date - MAY Social Security Payment Schedule 2026 in the USA Revealed")

![[Breaking News] Social Security Administration payment on 27th May 2026](https://dailyictpost.com/wp-content/uploads/2026/05/Breaking-News-Social-Security-Administration-payment-on-27th-May-2026-150x150.webp "[Breaking News] Social Security Administration payment on 27th May 2026")